Thorn received its Australian Credit Licence under the National Consumer Credit

Protection legislation in 2010, making it one of the first financial service providers in

Australia to be licensed. A key element of Thorn gaining its license was having a Responsible

Lending Policy under which Thorn seeks to ensure customers are treated fairly and provided

access to goods and services that meet their needs and budget. Within Thorn’s policy are

hardship provisions which are intended to help customers cope with unforeseen circumstances.

A large component of Thorn’s consumer customer base comprises Australians who are excluded from

the financial mainstream and it has become increasingly apparent that this is a substantial

group:

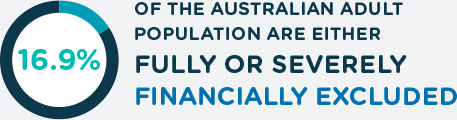

- 16.9 per cent of the Australian adult population, or just over 3 million people, are either

fully or severely financially excluded

- 42.9 per cent of the Australian adult population, or 7.7 million people, are marginally

financially excluded

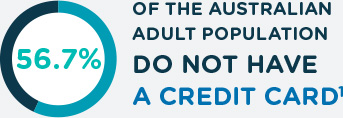

- 56.7 per cent of the Australian adult population, or over 10 million people, do not have a

credit card1

There are many reasons for financial exclusion but it is because of this situation that Thorn has

developed its “fair go” policy, enabling people to have access to household goods when there are

few alternatives.

1Connolly C, Measuring Financial Exclusion in Australia, Centre for Social Impact (CSI) – University of New South Wales, 2014, for National Australia Bank.

1Connolly C, Measuring Financial Exclusion in Australia, Centre for Social Impact (CSI) – University of New South Wales, 2014, for National Australia Bank.

THE “MUM TEST”

A feature of how Thorn operates when dealing with customers is to apply what we call the “Mum test”.

This means staff are encouraged to treat customers “as if they were your mum” and do whatever is

reasonable to assist them. We do this to ensure customers get a “fair go”, particularly people who

may have encountered difficulties in their lives.

HARDSHIP POLICY

Thorn also has a hardship policy in place, enabling customers to extend the balance of their contract

at a lower payment without any charges or penalties. This was recently used for one of our long

standing customers in Victoria who was not only battling health issues but had also lost her home

due to a fire. Under the hardship policy, Radio Rentals cleared her account, replaced the items she

had lost and ensured she would no longer have to make any payments.

In addition to fee free contract extensions Thorn also offers product downgrades without incurring

any penalties or additional fees, returns of unnecessary items without penalty, and relief on

payment commitments under its dedicated hardship program.